Credit card surcharge rules are shaping how small businesses handle payments today. Every time a customer taps or swipes a card, there is a cost behind it. That cost often feels small at first, but over time it adds up and starts cutting into margins.

So the real question is not just whether a fee can be added, but how to do it without getting into trouble. The answer sits inside credit card surcharge rules, and those rules are not the same everywhere.

What is a Credit Card Surcharge in Real Terms

Breaking it down simply

- A what is credit card surcharge question usually comes from businesses noticing higher payment costs

- It is a small extra fee added when a customer chooses to pay with a credit card

- That fee helps cover the merchant processing fee charged by banks and payment providers

Why it exists

- credit card processing rates are not fixed and often increase

- Businesses absorb these costs unless they pass them on

- A surcharge on credit card transactions helps balance that cost

Are Credit Card Surcharges Actually Legal

Straight answer

- Yes, but only if credit card surcharge rules are followed

- Federal law allows it, but states can control how it is used

What makes it legal

- The fee must reflect actual merchant credit card processing cost

- Customers must see it clearly before paying

- It must appear separately on the receipt

Missing even one of these points can turn a legal credit card surcharge into a violation.

The Rules That Apply Across the U.S.

Card network expectations

Payment networks like Visa and Mastercard have their own conditions.

- Maximum surcharge usually around 3 percent

- Advance notice required before applying fees

- Clear communication to customers

These are part of the broader credit card surcharge rules that every business must follow.

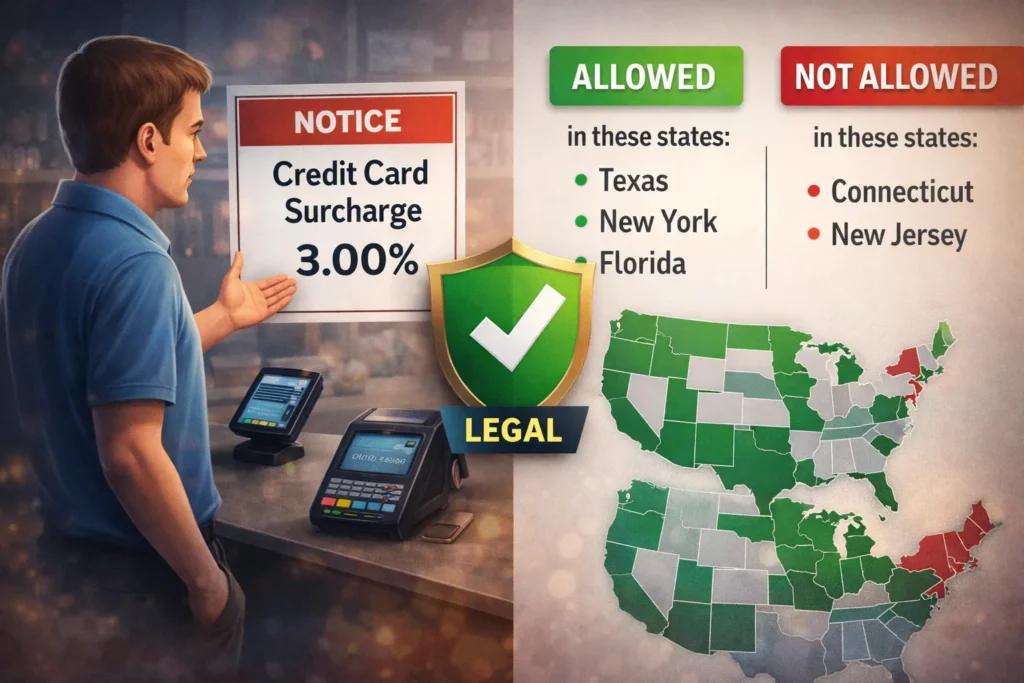

State-by-State Reality in 2026

This is where things get interesting. Not every state treats surcharges the same way.

States where surcharges are allowed

- Florida

- Texas

- New York

- Illinois

- Arizona

In these states, credit card surcharging is allowed, but only with full transparency and proper setup.

States where things feel unclear

- California

- New Jersey

- Massachusetts

Here, credit card surcharge laws by state have gone through legal changes. Businesses can still apply surcharges, but wording and presentation matter a lot.

States where surcharges are not allowed

- Connecticut

A surcharge on credit card payments is not permitted here, no matter the situation.

Simple Table for Quick Understanding

| Category | What it Means | Action Needed |

| Allowed | Most states | Follow credit card surcharge rules strictly |

| Restricted | CA, NJ, MA | Be careful with wording and display |

| Prohibited | CT | Do not apply surcharges |

How Much Can Be Charged Without Risk

Staying within limits

- Must match actual merchant credit card processing cost

- Usually capped at 3 percent

Why this matters

Charging more than allowed is one of the fastest ways to break credit card surcharge rules and face penalties.

Surcharge vs Convenience Fee Explained Clearly

Surcharge

- Only applies to credit card payments

- Directly tied to credit card processing rates

Convenience fee

- Charged for using a certain payment method or channel

- Not limited to credit cards

Mixing these up can lead to problems with credit card surcharge rules.

How to Add a Surcharge Without Complications

What needs to be done

- Inform the payment processor

- Notify card networks

- Place clear signs at checkout

- Show the fee separately on receipts

Doing this properly ensures a smooth and legal credit card surcharge setup.

Mistakes That Cause Problems Quickly

Lack of clear communication

- Customers must know upfront

Overcharging

- Must stay within actual merchant credit card processing cost

Charging on debit cards

- Not allowed under credit card surcharge rules

How Customers Usually React

What tends to happen

- Some customers switch to cash

- Some accept the fee without concern

- Confusion happens when fees are not explained

What works better

- Simple explanation

- Small percentage

- Honest pricing approach

When Adding a Surcharge Makes Sense

Good situations

- Businesses with tight margins

- High volume transactions

- Increasing credit card processing rates

Situations to rethink

- Premium customer experience businesses

- Highly competitive pricing environments

What is Changing in 2026

Current direction

- More businesses using surcharges

- Customers becoming more aware

- Laws getting clearer over time

What to expect next

- Stronger enforcement of credit card surcharge rules

- More updates in credit card surcharge laws by state

- Higher focus on transparency

Conclusion:

Credit card surcharge rules are not something to ignore or guess through. They define how businesses recover costs without damaging trust or facing penalties.

Understanding how a surcharge on credit card transactions works, where it is allowed, and how to apply it correctly makes all the difference.

Done right, it protects margins. Done wrong, it creates problems.

Frequently Asked Questions

What is a surcharge fee?

A what is a surcharge fee explanation comes down to a small added cost when paying by credit card, designed to cover processing charges while staying within defined legal limits.

Are credit card surcharges allowed in every state?

No, credit card surcharge laws by state vary. Most states allow them under credit card surcharge rules, but some restrict or ban them completely.

What is the maximum surcharge allowed?

The fee must not exceed the real merchant processing fee, and usually stays within a 3 percent cap under standard credit card surcharge rules.

Can businesses charge surcharges on debit cards?

No, a surcharge on credit card transactions is allowed, but debit card surcharges are not permitted under current credit card surcharge rules.

Do customers need to be informed before paying?

Yes, clear notice is required before payment. Transparency is a key part of following credit card surcharge rules correctly.

Is there a difference between surcharge and convenience fee?

Yes, a surcharge applies only to credit cards, while a convenience fee applies to specific payment methods, making them different under credit card surcharge rules.

Why do businesses use credit card surcharges?

Businesses use them to recover rising credit card processing rates and reduce the burden of merchant credit card processing costs.

What happens if surcharge rules are not followed?

Breaking credit card surcharge rules can result in penalties, fines, and even losing access to card payment systems.

Do surcharges affect customer experience?

Yes, but when explained clearly and kept reasonable, most customers accept credit card surcharging without major concerns.

Will surcharge laws continue to change?

Yes, updates in credit card surcharge laws by state are expected as digital payments grow and regulations continue to evolve.