Businesses face tough choices with payment processing fees eating into profits, so understanding cash discount vs surcharge options helps decide the best path forward.

What is a Cash Discount Program?

A cash discount program lets merchants list a higher price but give a discount to customers paying with cash or debit, covering credit card costs without direct fees. This setup turns standard pricing into an incentive for non-credit payments, often leading to zero cost credit card processing for the business when customers switch. Merchants love how it shifts the burden subtly while keeping everyone happy.

What is a Surcharge Program?

Surcharge programs add an extra fee only to credit card transactions, passing processing costs straight to those users. Customers see the full price upfront, then a surcharge tacked on for cards, which must stay under 4% federally but follows state caps. Online setups need clear notices before checkout to avoid issues with surcharge online payments.

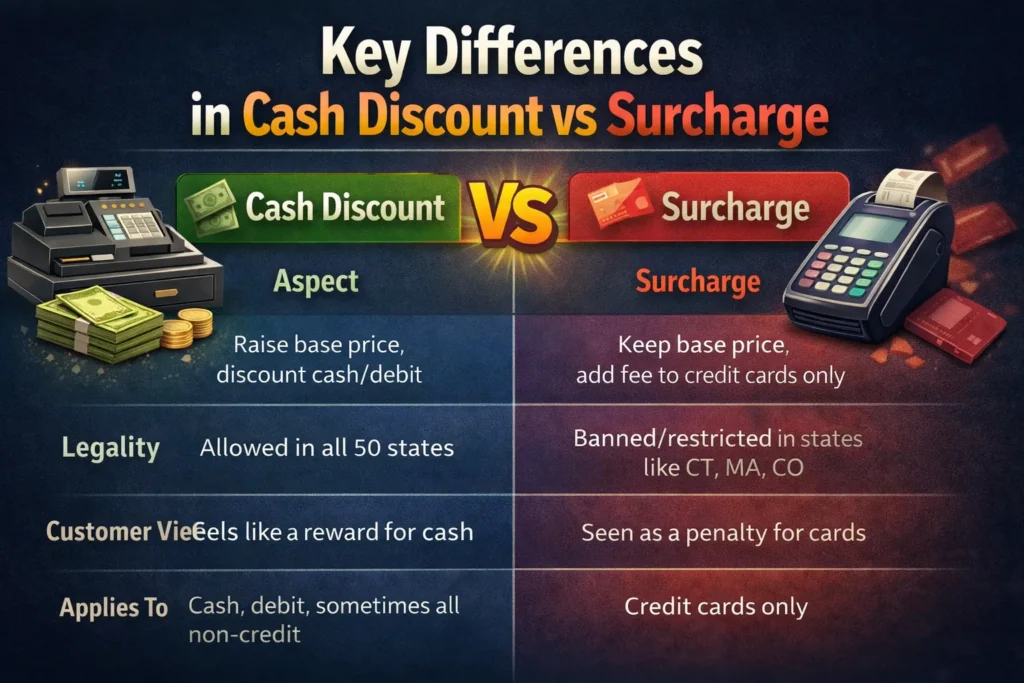

Key Differences in Cash Discount vs Surcharge

| Aspect | Cash Discount Program | Surcharge Program |

| Pricing Approach | Raise base price, discount cash/debit | Keep base price, add fee to credit cards only |

| Legality | Allowed in all 50 states | Banned/restricted in states like CT, MA, CO |

| Customer View | Feels like a reward for cash | Seen as a penalty for cards |

| Applies To | Cash, debit, sometimes all non-credit | Credit cards only |

Cash discount vs surcharge boils down to incentives versus direct charges, with each fitting different business needs.

Legal Rules for Credit Card Surcharge

Credit card surcharge rules demand clear signage at entrances and receipts, plus caps matching actual costs. States like Nevada limit to 1.5%, while Texas blocks surcharges but allows convenience fees. For merchant cash discount program setups, federal laws like the Durbin Amendment back incentives nationwide, making compliance simpler.

Pros and Cons of Each Approach

Cash Discount Benefits

- Cuts fees by up to 90%, aiming for zero cost credit card processing.

- Builds loyalty as customers chase savings.

- Works everywhere, no state bans.

Cash Discount Drawbacks

- Needs price adjustments, which confuse some shoppers.

- Less effective if cash use stays low.

Surcharge Benefits

- No price changes needed, quick setup.

- Recovers full fees from card users.

- Boosts margins fast for high-volume spots.

Surcharge Drawbacks

- State restrictions limit use.

- Risks customer pushback on extra charges.

Comparing Costs: Which Saves More?

Cash discount vs surcharge often favors cash discounts for nationwide flexibility and debit inclusion, saving $15,000-$20,000 yearly on $500k volume. Surcharges shine where legal, fully offloading credit fees without repricing.

Small businesses see bigger wins with cash discount vs surcharge via cash discounts due to fewer rules, while online sellers weigh surcharge online payments carefully.

| Savings Example ($100 Sale, 3% Fee) | Cash Discount | Surcharge |

| Card Payment | Business gets full $100 (fee built-in) | Customer pays $103, business $100 |

| Cash Payment | Customer pays $97, business $97 | Customer pays $100, business $100 |

| Annual Savings (1,000 sales) | Up to $2,900 | Up to $3,000 (if all cards) |

Implementing a Merchant Cash Discount Program

Start by checking local rules, then set a 2-4% discount matching fees.

Update POS for auto-discounts, add signs like “Pay cash, save 3%!” and train staff.

Track uptake monthly to tweak for max zero cost credit card processing.

Setting Up Surcharge Programs

Post notices everywhere, register with card networks, cap at your cost.

For surcharge online payments, add pre-checkout warnings and receipt lines.

Providers handle tech, ensuring compliant terminals.

Conclusion:

Cash discount vs surcharge tilts to cash discounts for small shops, legal everywhere, encourages cash flow. Surcharges suit service pros with big card tickets, but skip banned states. Test both if possible, as the merchant cash discount program edges out for simplicity.

Frequently Asked Questions

What exactly is cash discount vs surcharge difference?

Cash discount vs surcharge means cash discounts reward non-card payments by lowering the price from a base, while surcharges add fees only to credit cards. Cash works nationwide; surcharges face state limits. Saves businesses fees either way, but pick by your setup and customers.

Is a cash discount program legal everywhere?

Yes, cash discount program options stay legal in all 50 states under federal rules like Durbin Amendment. No caps on amounts if disclosed clearly. Great for consistent use across locations without worry.

What are main credit card surcharge rules?

Credit card surcharge rules require fees under 4%, apply to credit only—not debit—plus signs and receipts. Banned in states like Massachusetts, Connecticut. Always disclose before sale.

Can surcharge online payments?

Yes, but surcharge online payments need advance notice on site before checkout and on confirmations. Follow same caps and credit-only rules. Comply to dodge fines.

How does merchant cash discount program save money?

A merchant cash discount program absorbs fees into pricing, lets cash payers save, cuts your costs 90% via switches. Example: $1,000 monthly fees drop to $100. Boosts profits fast.

What’s zero cost credit card processing?

Zero cost credit card processing happens when programs like cash discounts pass all fees to users indirectly, so business pays nothing. Providers automate it fully.

Cash discount vs surcharge, which for small biz?

Cash discount vs surcharge favors cash discounts for small businesses—universal legality, positive customer feel. Surcharges good for high-card volumes where allowed. Test yours.

Any surcharge programs downsides?

Surcharge programs risk customer anger over fees, state bans in 6+ places, and debit exclusion. Needs perfect disclosure or fines hit.

Steps for cash discount vs surcharge setup?

For cash discount vs surcharge, assess laws, pick matching your state/customers, update POS/signage, monitor savings. Cash easier start.

Does cash discount vs surcharge affect loyalty?

Cash discount vs surcharge sees discounts build loyalty via savings feel, surcharges sometimes annoy. Discounts win customer vibes long-term.