Merchant cash advance is a financing option many businesses turn to when they need fast cash without jumping through hoops. It’s not your typical bank loan. Instead of borrowing money and paying interest over a fixed term, a merchant cash advance gives you funds upfront and lets you pay it back through a percentage of your daily sales.

This makes it flexible for businesses that have fluctuating revenue, like seasonal stores, restaurants, or small startups.

Think of it as a cash flow booster that moves with your business, when sales are high, you pay a bit more, when sales are slow, payments adjust. But like anything, it has pros, cons, and things you need to watch closely.

What is a Merchant Cash Advance?

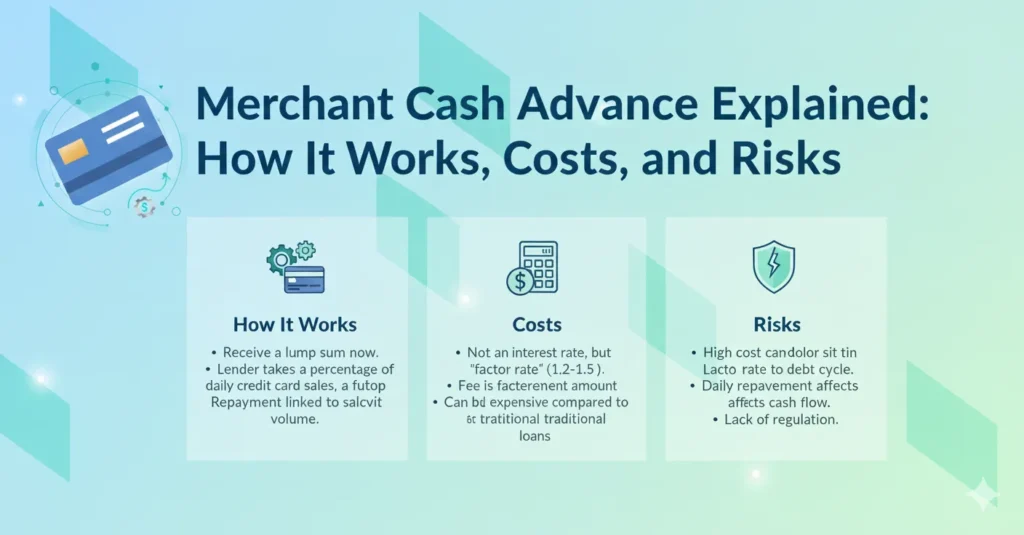

Simply put, a merchant cash advance is an advance on your future sales. A provider gives you money now, and you repay it with a slice of your daily credit card or debit card revenue.

- Perfect for seasonal businesses, where income spikes at certain times of the year

- Faster than banks, you could have funds in 24–48 hours

- No fixed monthly payments, repayments adjust based on actual sales

It’s important to note that this isn’t a loan in the traditional sense. There’s no interest rate like banks offer. Instead, you pay back the advance plus a factor rate.

How Merchant Cash Advance Works

Here’s a clear picture of how merchant cash advance works:

- Apply: Businesses usually fill out a simple online application. They’ll provide recent credit card statements or bank deposits.

- Approval: Providers quickly review sales history. Since repayment is tied to sales, they care more about revenue than credit score.

- Get Funded: Funds hit your account—sometimes the same day or the next business day.

- Repay: A fixed percentage of your daily sales is automatically deducted until the full advance plus fees are paid.

- Optional Settlement: If payments become unmanageable, businesses sometimes use merchant cash advance settlement companies to negotiate or reduce debt.

| Feature | Details |

| Funding Amount | $5,000 – $500,000+ depending on sales history |

| Repayment Term | Typically 3–18 months |

| Payment Method | Percentage of daily credit card sales |

| Costs | Factor rates 1.1–1.5 (not APR) |

| Best For | Seasonal businesses, small businesses, startups |

Costs and Factor Rates

The cost of a merchant cash advance can be surprising if you’re new to it. Instead of interest rates, MCAs use factor rates.

For example:

- If you take $50,000 with a factor rate of 1.3, you repay $65,000.

- Payments are daily and tied to sales, so during slow periods, the deduction is smaller.

Additional fees might include processing or origination fees. That’s why comparing providers is important. Don’t just look at the upfront amount; look at total repayment and the impact on your cash flow.

Risks to Consider

MCAs are flexible, but they come with risks you can’t ignore:

- High cost: MCAs are often more expensive than traditional loans

- Cash flow strain: Daily deductions can feel heavy during slow months

- Limited oversight: Merchant cash advance regulation is not uniform across states

- Settlement risks: Only use trusted merchant cash advance settlement companies if negotiating

It’s like borrowing from tomorrow’s sales—you get cash now but commit a slice of your future income.

Who Should Consider a Merchant Cash Advance?

A merchant cash advance for small businesses or startups makes sense if you:

- Have reliable daily card sales

- Need quick cash for inventory, equipment, or marketing

- Operate in seasonal industries where sales spike periodically

For startups, this can be a lifeline to cover operational costs before revenue stabilizes.

Merchant Cash Advance Software

Running an MCA without tools is like driving blind. Merchant cash advance software helps businesses:

- Track repayments automatically

- Forecast cash flow impact

- Manage multiple MCAs if you have more than one

Pair it with secure payment processing and online merchant services for smooth operations.

Tips for Managing Your MCA

- Know your factor rate and total repayment before signing

- Keep cash reserves for slow periods

- Monitor daily deductions to avoid surprises

- Use merchant cash advance settlement companies only when necessary

- Treat the advance as a bridge, not a long-term solution

Real-Life Example

Imagine a small bakery. Holiday season approaches, and the bakery needs $20,000 to stock up on ingredients and hire temporary staff. They take a merchant cash advance. Their daily sales are $2,000, and the provider takes 10% daily. Payments fluctuate:

- On a $2,500 sales day, $250 is deducted

- On a $1,500 sales day, $150 is deducted

This flexibility ensures the bakery can manage cash flow without missing critical sales opportunities.

Conclusion:

A merchant cash advance is a flexible, fast financing solution for businesses that need cash now and have predictable sales. It’s ideal for seasonal businesses, startups, and small businesses. While it’s convenient, the high cost and cash flow impact mean careful planning is essential. Always pair it with secure payment processing and reliable online merchant services to protect your business.

Frequently Asked Questions

How does a merchant cash advance work?

Funds are given upfront, repaid through a percentage of daily sales.

Is a merchant cash advance a loan?

No, it’s an advance on future revenue, not a traditional loan.

Who benefits most from MCAs?

Small businesses, startups, and seasonal businesses with consistent card sales.

How quickly can I get funding?

Funding can happen in 24–48 hours after approval.

What are factor rates?

A factor rate determines the total repayment, usually between 1.1 and 1.5.

Are MCAs regulated?

Regulation varies by state; there’s no federal oversight.

Can I settle early?

Yes, through merchant cash advance settlement companies, but fees may apply.

How do I track repayment?

Use merchant cash advance software or your merchant account reporting.

What risks should I watch?

High costs, cash flow strain, and settlement risks.

Can startups qualify for MCAs?

Yes, if daily card sales or revenue projections are sufficient.